India’s Semiconductor Infrastructure Push Is Triggering a New Era of Global Investment, Manufacturing Migration, and Strategic Technology Realignment

The global semiconductor industry is no longer operating under the assumptions that defined the past three decades.

The old globalization model—built on concentrated manufacturing efficiency, low-cost production dependency, and hyper-centralized supply chains—is now being systematically dismantled by geopolitical fragmentation, technology nationalism, supply-chain shocks, AI-driven compute demand, and rising concerns over strategic technological sovereignty.

What the world is witnessing today is not merely a semiconductor expansion cycle.

It is the restructuring of global industrial power.

And increasingly, global investors, semiconductor giants, sovereign funds, strategic policymakers, and multinational technology companies are placing India at the center of that transition.

From Washington to Tokyo, from Taiwan to the Gulf, from Silicon Valley boardrooms to sovereign investment committees in the Middle East and Europe, India is rapidly emerging as one of the world’s most strategically trusted semiconductor destinations.

According to iBluu Consulting Venture Private Limited (iBCV), a venture of iBluu Corporations, the accelerating global interest in India’s semiconductor ecosystem reflects a much deeper geopolitical and industrial shift—one where nations are no longer investing only in markets, but in resilient technological alliances and trusted manufacturing geographies.

The Semiconductor Industry Has Become the Foundation of Strategic Global Power

Semiconductors are no longer a conventional industrial product category.

They are now the foundational infrastructure behind:

- Artificial Intelligence systems

- Defense electronics

- Aerospace technologies

- Quantum computing

- Advanced telecommunications

- Electric vehicles

- Renewable energy systems

- Cloud infrastructure

- Robotics and industrial automation

- National digital security architecture

This is precisely why the semiconductor industry is increasingly being treated as a matter of economic sovereignty and national security.

The global semiconductor market is projected to exceed approximately $1 trillion by the early 2030s, driven by explosive demand from AI infrastructure, data centers, edge computing, autonomous mobility, industrial IoT, and next-generation digital systems.

Yet while demand is becoming global, supply chains remain dangerously concentrated.

More than 75% of advanced semiconductor manufacturing capacity remains heavily concentrated in East Asia, particularly Taiwan, South Korea, and parts of China.

That concentration is now viewed as one of the greatest structural vulnerabilities in the modern global economy.

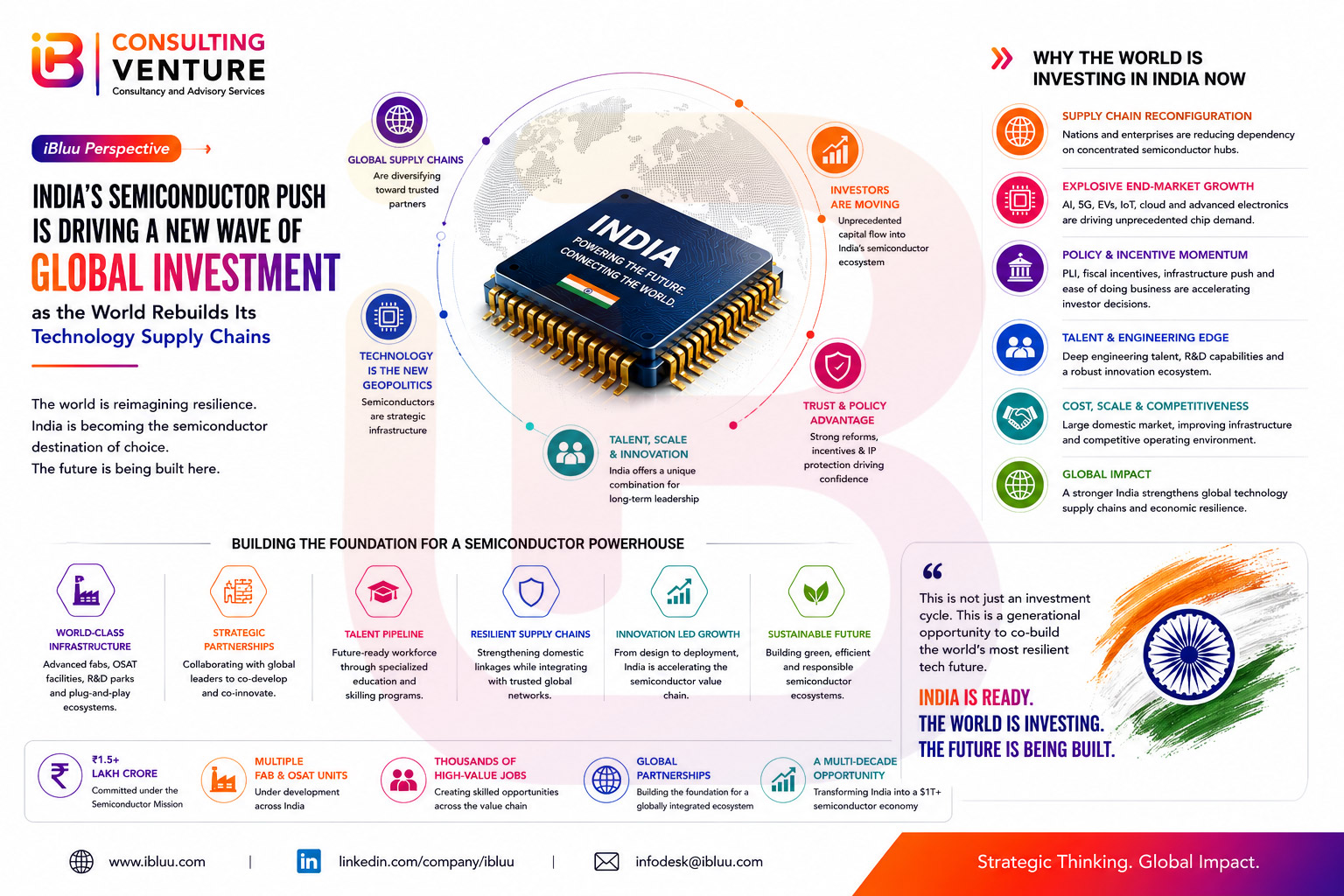

Why the World Is Repositioning Semiconductor Investment Toward India

1. India Is Viewed as a Trusted Strategic Geography

Global investors are no longer evaluating semiconductor ecosystems solely through labor economics or manufacturing costs.

They are evaluating:

- Geopolitical reliability

- Democratic institutional continuity

- Diplomatic stability

- Long-term policy predictability

- Strategic alliances

- Supply-chain resilience

- Technology-security alignment

India scores strongly across all these dimensions.

Unlike several manufacturing-heavy economies facing geopolitical uncertainties, India is increasingly being viewed as a stable strategic bridge between Western economies, Asian supply chains, Gulf capital, and emerging industrial markets.

This has significantly elevated India’s credibility among:

- U.S. technology firms

- Japanese semiconductor players

- Taiwanese chip manufacturers

- European industrial investors

- Gulf sovereign wealth funds

For global investors, India increasingly represents a “trusted diversification geography” rather than merely a low-cost manufacturing location.

That distinction is strategically critical.

2. India Has Something Most Semiconductor Economies Lack — Domestic Scale

One of India’s greatest structural advantages is that it is simultaneously:

- A large consumption economy

- A large talent economy

- A rising manufacturing economy

- A rapidly digitizing economy

India’s electronics market is expected to cross approximately $400 billion in the coming years, while semiconductor demand is projected to increase dramatically across:

- Smartphones

- AI infrastructure

- Consumer electronics

- EV manufacturing

- Telecom systems

- Renewable energy systems

- Industrial automation

- Defense electronics

Most semiconductor economies are either manufacturing-led or consumption-led.

India has the potential to become both.

That dual-engine advantage is one of the primary reasons global semiconductor capital is increasingly moving toward India.

3. The “China Plus One” Strategy Is Accelerating Faster Than Expected

The global semiconductor industry has fundamentally changed its investment philosophy after:

- COVID-era disruptions

- U.S.–China technology tensions

- Taiwan Strait concerns

- Export-control restrictions

- Red Sea shipping disruptions

- Global logistics bottlenecks

As a result, semiconductor companies are aggressively diversifying manufacturing risk.

The “China Plus One” strategy is no longer optional.

It is now institutional strategy.

India has emerged as one of the few countries capable of supporting long-term diversification at scale because of:

- Market size

- Talent availability

- Industrial land availability

- Infrastructure upgrades

- Government incentives

- Geopolitical positioning

- Engineering ecosystem depth

This explains why international semiconductor firms are increasingly expanding engagement across India’s semiconductor ecosystem.

India’s Semiconductor Infrastructure Is Transitioning from Vision to Execution

One of the most important changes in global investor perception is that India’s semiconductor ambitions are no longer being viewed as theoretical policy declarations.

Execution has begun.

India’s semiconductor ecosystem is now witnessing real infrastructure deployment across multiple states.

Major Semiconductor Ecosystem States in India

| State | Strategic Semiconductor Focus |

|---|---|

| Gujarat | Semiconductor fabrication, ATMP/OSAT, electronics manufacturing |

| Assam | Semiconductor packaging and assembly ecosystem |

| Karnataka | Chip design, AI, R&D and innovation infrastructure |

| Tamil Nadu | Electronics manufacturing and industrial integration |

| Telangana | Fabless ecosystem and semiconductor innovation |

| Uttar Pradesh | Electronics manufacturing and device ecosystems |

| Maharashtra | Advanced industrial electronics and manufacturing |

Major investments and ecosystem participation now involve:

- Tata Electronics

- Micron Technology

- CG Power

- Renesas Electronics

- Tower Semiconductor-linked collaborations

- Applied Materials ecosystem participation

- Multiple OSAT and ATMP infrastructure players

The Micron Technology semiconductor assembly and testing facility in Gujarat alone represents one of the largest and most strategically symbolic semiconductor investments in India’s industrial history.

Why Global Semiconductor Giants Trust India’s Long-Term Potential

According to iBCV’s strategic analysis, global semiconductor firms increasingly trust India because of six structural strengths.

A. India Already Powers the Global Semiconductor Design Ecosystem

India is not entering semiconductors from zero.

The country already plays a major role in global chip design and engineering services.

A significant percentage of the world’s semiconductor design talent already operates from India through multinational R&D and engineering centers.

This creates a strong foundation for future manufacturing integration.

B. India Has One of the World’s Largest Engineering Talent Pipelines

India produces one of the world’s largest annual pools of engineers and technology professionals.

As AI, advanced computing, and semiconductor systems become more complex, talent depth becomes a strategic advantage.

Global companies understand this.

C. India’s Infrastructure Story Is Improving Rapidly

Semiconductor manufacturing requires:

- Reliable power

- Water infrastructure

- Logistics efficiency

- Port connectivity

- Industrial ecosystems

- Transport integration

- Renewable energy access

India’s broader infrastructure transformation—including Dedicated Freight Corridors (DFC), industrial corridors, logistics parks, smart industrial cities, port modernization, renewable energy growth, and digital infrastructure expansion—is significantly improving investor confidence.

D. India Is Becoming an AI and Data Infrastructure Market

Semiconductors are no longer driven only by consumer electronics.

AI infrastructure is now becoming one of the largest semiconductor demand drivers globally.

India’s growing digital economy, cloud expansion, AI ecosystem, fintech scale, and data center investments strengthen its semiconductor relevance significantly.

E. Global ESG and Sustainability Trends Favor India

India’s renewable energy expansion is becoming another strategic advantage.

Semiconductor facilities are energy-intensive operations.

Global investors increasingly prefer semiconductor ecosystems aligned with:

- Renewable power access

- Carbon transition goals

- Long-term ESG alignment

India’s renewable infrastructure growth improves its attractiveness substantially.

F. India Is Emerging as a Strategic Manufacturing Counterweight

Global industrial powers increasingly prefer multipolar manufacturing ecosystems.

No major economy wants excessive concentration risk in a single geography anymore.

India is increasingly viewed as the most scalable democratic manufacturing alternative capable of balancing future technology supply chains.

Global Capital Is No Longer Ignoring India

The scale of global semiconductor-linked investment discussions involving India has expanded rapidly over the past few years.

This includes interest from:

- Sovereign wealth funds

- Strategic infrastructure investors

- Semiconductor equipment manufacturers

- Electronics supply-chain firms

- AI infrastructure companies

- Private equity funds

- Deep-tech capital platforms

- Institutional manufacturing investors

What is changing is not just investment quantity.

It is investment conviction.

The world increasingly believes India can become indispensable within the future semiconductor ecosystem.

The Real Strategic Question Is Bigger Than Semiconductors

According to J Parasher, Founder and Managing Director of iBluu Corporations, the semiconductor transition should not be viewed narrowly as a manufacturing sector opportunity.

It is a strategic civilizational transition.

“The semiconductor race is ultimately about who controls the infrastructure powering the next industrial era,” Parasher notes. “Countries that build semiconductor ecosystems will influence AI capability, digital sovereignty, advanced manufacturing strength, defense technologies, and future economic power.”

This is why semiconductors are now directly linked to:

- National competitiveness

- Strategic autonomy

- Export capability

- Technological leadership

- Geopolitical influence

- Industrial resilience

Risks and Structural Challenges Still Remain

Despite strong optimism, global investors remain cautious about several factors:

- High capital intensity

- Water dependency

- Supply-chain localization challenges

- Technology-transfer limitations

- Long project gestation periods

- Talent specialization gaps

- Global cyclical semiconductor demand fluctuations

India’s long-term success will depend on synchronized execution between:

- Central government

- State governments

- Global technology partners

- Infrastructure developers

- Capital providers

- Energy systems

- Educational ecosystems

Execution consistency will determine whether India evolves into a global semiconductor powerhouse or remains partially integrated into the value chain.

iBluu Perspective: India Is Becoming Part of the Foundation of the Next Global Technology Order

The global semiconductor industry is no longer searching only for efficiency.

It is searching for resilience, trust, strategic stability, and scalable industrial ecosystems.

India increasingly satisfies all four.

This is why global investment momentum toward India is accelerating.

The world is rebuilding its technology supply chains.

And for the first time in modern industrial history, India is no longer standing at the edge of the semiconductor economy.

It is steadily moving toward the center of it.

About iBCV — iBluu Consulting Venture Private Limited

iBluu Consulting Venture Private Limited (iBCV), a venture of iBluu Corporations, operates across strategic consulting, infrastructure advisory, investment consulting, industrial partnerships, technology ecosystem advisory, government engagement, mergers and acquisitions support, and long-horizon economic transformation strategy.

The analytical depth reflected in this article is shaped by the strategic framework of J Parasher, Founder and Managing Director of iBluu Corporations, whose work focuses on industrial competitiveness, infrastructure economics, technology ecosystems, global investment realignment, and national capability-building models.

Disclaimer: This article is intended solely for informational, strategic insight, and industry analysis purposes. The views expressed are based on publicly available information, industry trends, market developments, and analytical interpretation as of 2026. This document does not constitute financial advice, investment recommendation, legal guidance, or policy endorsement. Readers, investors, and institutions are advised to conduct independent due diligence and consult professional advisors before making any strategic or financial decisions.