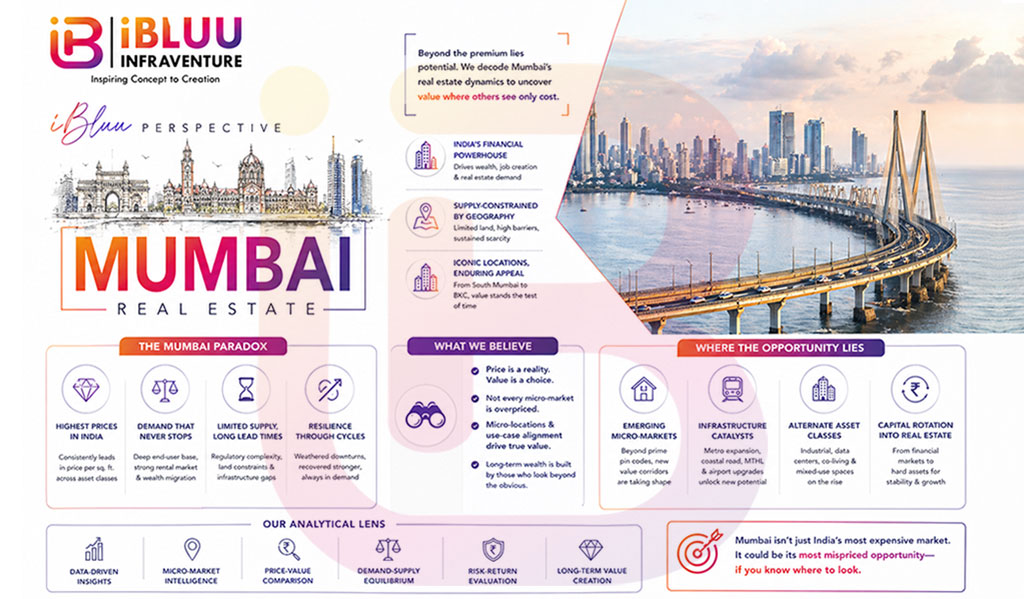

iBluu Perspective: Mumbai Real Estate Outlook — India’s Most Expensive Market

The real estate market of Mumbai is no longer just India’s most expensive—it is its most structurally complex and globally relevant urban asset class.

Unlike emerging markets driven by expansion, Mumbai operates on a scarcity premium model—finite land, extreme demand concentration, and deep capital inflows. Prices are not merely rising; they are being continuously repriced by capital, infrastructure, and global investor participation.

iBluu View:

Mumbai is transitioning from a real estate market into a capital preservation and global wealth allocation zone. The question is no longer “Is Mumbai expensive?”

The real question is: Is Mumbai underpriced relative to its global positioning?

1. Demand Dynamics: Investment vs Self-Use — A Capital-Driven Market

Mumbai’s demand structure has undergone a decisive shift:

- 60–70% demand in premium/mid-luxury segments is investor-led

- End-user demand remains dominant in peripheral and mid-income segments

- Ultra-luxury (₹25 crore+) is primarily capital allocation, not residential consumption

Key Insight:

Mumbai is increasingly behaving like London or New York, where real estate is a financial instrument first, residential asset second.

2. Land Economics: The Core Driver of Price Escalation

Mumbai’s pricing is fundamentally dictated by land cost intensity, among the highest globally.

Top Land Price Benchmarks (Indicative 2025–26)

| Location | Land Price Range (₹ Cr per acre) | Market Position |

|---|---|---|

| South Mumbai (Malabar Hill, Cuffe Parade) | 500–1,200+ | Ultra-prime global luxury |

| Bandra West / Khar | 300–700 | Premium lifestyle hub |

| Lower Parel / Worli | 250–600 | Financial + luxury convergence |

| Powai | 150–300 | Integrated township premium |

| Thane (Select micro-markets) | 80–180 | Emerging investment corridor |

Implication:

High entry barriers ensure sustained price resilience, even during downturn cycles.

3. Ultra-Luxury vs Affordable: A Market of Extremes

Mumbai is a bifurcated market—where wealth concentration drives one segment, and affordability constraints suppress the other.

- Ultra-luxury pricing (South Mumbai): ₹1.2–2.5 lakh per sq. ft.

- Mid-tier suburbs: ₹25,000–60,000 per sq. ft.

- Peripheral zones (Thane, Navi Mumbai): ₹8,000–25,000 per sq. ft.

Observation:

The price gap is not a distortion—it is structural, reflecting income inequality, capital concentration, and location scarcity.

4. Heritage Properties: The Silent Premium Asset Class

Mumbai’s heritage real estate (Colaba, Fort, Byculla precincts) operates in a niche but high-value segment:

- Price range: ₹40,000–1,50,000 per sq. ft. (depending on redevelopment potential)

- Increasing interest from family offices and boutique investors

iBluu Insight:

Heritage assets are evolving into “cultural capital investments”—low liquidity, high prestige, long-term upside.

5. Infrastructure as a Price Multiplier

Mumbai’s next growth wave is infrastructure-led repricing.

Key Catalysts:

- Mumbai Trans Harbour Link

- Coastal Road Project

- Metro Lines (Phase II & III expansion)

- Navi Mumbai International Airport

Impact:

- 20–40% price appreciation potential in connected corridors

- Strong upside in Navi Mumbai, Chembur, Wadala, Panvel

6. Buyer Geography: Where Capital Is Moving

Top Preferred Investment Zones:

- Bandra–Worli Sea Link belt

- Lower Parel / Worli (financial district proximity)

- Powai (integrated urban ecosystem)

- Thane & Navi Mumbai (value + infrastructure play)

Trend:

Buyers are shifting from location prestige to ecosystem value—connectivity, lifestyle, and future appreciation.

7. Commercial Real Estate: India’s Financial Engine

Mumbai remains India’s undisputed commercial capital.

- Grade A office pricing: ₹25,000–70,000 per sq. ft.

- Rental yields: 6–9% (higher than residential)

- Key hubs: BKC, Lower Parel, Nariman Point

Insight:

Institutional investors (REITs, sovereign funds) are increasing exposure to Mumbai office assets, driven by stable cash flows.

8. Global Capital: NRI, HNI, and Institutional Flows

Mumbai attracts disproportionate global capital:

- Strong NRI demand from Middle East, UK, US

- HNIs allocating 20–30% of portfolios into real estate

- Private equity and sovereign funds targeting commercial + luxury residential

Structural Advantage:

Mumbai offers currency hedge + asset appreciation + rental yield combination.

9. Risk Assessment: The Structural Constraints

Despite its strengths, Mumbai faces critical risks:

- Affordability stress in mid-income segment

- Regulatory delays and approval complexity

- Infrastructure execution lag (timeline risk)

- High stamp duty and transaction costs

Risk Probability (2026–2030):

- Moderate correction risk: 20–25% probability

- Liquidity slowdown (mid-market): 30–35% probability

10. Scenario Outlook (2026–2035)

Base Case (Most Likely)

- CAGR: 8–10%

- Luxury outperforms mid-income

- Infrastructure-led corridors dominate growth

Upside Case

- CAGR: 12–15%

- Strong foreign capital inflows

- Mumbai strengthens position as Asia’s wealth hub

Downside Case

- CAGR: 5–7%

- Interest rate pressure + affordability constraints

11. Strategic Recommendations (Investor Playbook)

For Investors

- Allocate 50–60% to commercial assets (yield stability)

- Deploy 30–40% in luxury residential (capital appreciation)

- Target infrastructure-linked micro-markets early

For Developers

- Focus on premium + ultra-luxury segments

- Integrate lifestyle + green infrastructure positioning

For Policymakers

- Simplify approvals

- Rationalize transaction costs

- Accelerate infrastructure execution timelines

The iBluu Perspective: Mumbai Is Not Expensive—It Is Evolving

Mumbai is not a conventional market.

It is a capital city in the truest sense—not politically, but financially.

The next decade will not be defined by:

- Who builds more

- Or who sells faster

It will be defined by:

- Who understands capital flows

- Who aligns with infrastructure-led growth

- Who builds for global wealth, not local demand

Role of iBIV (iBluu InfraVenture Private Limited)

iBluu InfraVenture Private Limited, a venture of iBluu Corporations operates at the intersection of real estate intelligence, capital advisory, and strategic execution.

From investment advisory and M&A structuring to government engagement and market intelligence, iBIV enables clients to navigate complex markets like Mumbai with precision and strategic clarity.

The analytical depth of this report is shaped by the strategic lens of J Parasher, whose work focuses on long-term economic transformation, capital systems, and global benchmarking frameworks.

Conclusion: A Market That Will Define India’s Wealth Geography

Mumbai is not just India’s most expensive real estate market.

It is:

- A store of wealth

- A global capital magnet

- A strategic urban asset

And those who understand its structure early—

Will not just participate in the market.

They will define its next phase.

Disclaimer: This article is intended solely for informational and strategic insight purposes and does not constitute financial, investment, or legal advice. All data points are based on industry estimates, publicly available sources, and market intelligence as of 2025–2026. Readers and investors are advised to conduct independent due diligence and consult professional advisors before making any investment decisions. iBluu InfraVenture Private Limited (iBIV) and iBluu Corporations do not assume any liability for actions taken based on this analysis.