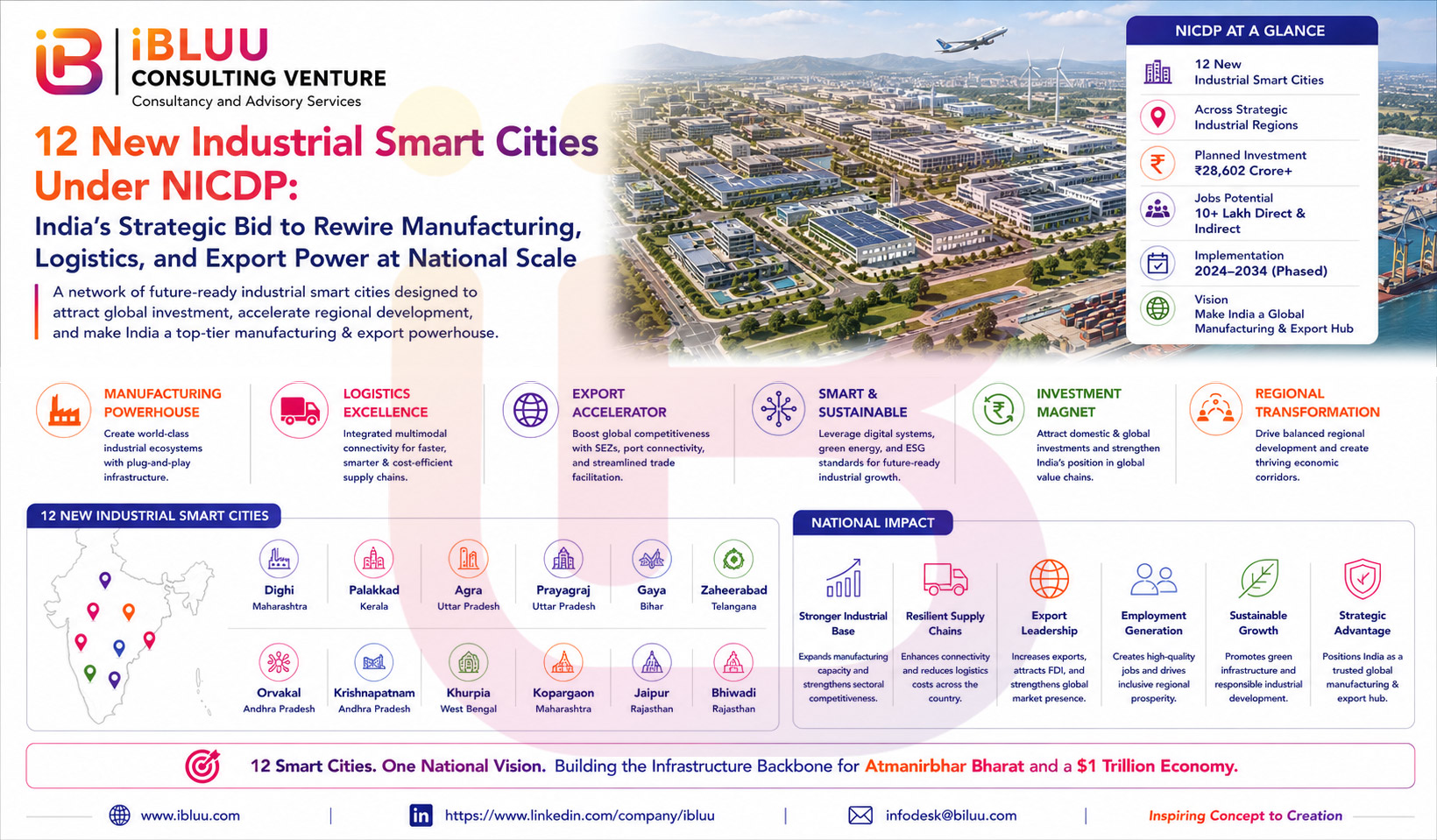

India’s 12 Industrial Smart Cities Under NICDP: The National Infrastructure Blueprint Powering India’s Rise as a Global Manufacturing and Logistics Powerhouse

For decades, India’s industrial expansion was constrained by fragmented logistics, delayed land aggregation, inadequate urban planning, unstable utility infrastructure, and policy execution gaps that diluted manufacturing competitiveness against China, Vietnam, South Korea, and increasingly, the Gulf-led industrial platforms emerging across the Middle East.

The launch and acceleration of 12 new industrial smart cities under the National Industrial Corridor Development Programme (NICDP) signals something fundamentally different.

This is not conventional industrial development.

It is a strategic redesign of India’s manufacturing geography.

Positioned across six major industrial corridors and 10 states, these greenfield industrial smart cities represent one of the most ambitious infrastructure-led industrialization programs in modern India — combining multimodal logistics integration, “plug-and-play” manufacturing ecosystems, smart urbanization, utility resilience, export orientation, and supply-chain acceleration into a single coordinated economic architecture.

At stake is far more than industrial land monetization.

India is attempting to structurally reposition itself within the global manufacturing order.

And the implications for capital markets, logistics, exports, real estate, industrial production, labor migration, and geopolitical supply-chain realignment are profound.

The 12 Industrial Smart Cities: India’s New Manufacturing Geography

The smart cities are strategically distributed across major industrial corridors and logistics networks to create synchronized industrial growth clusters.

The proposed cities include:

- Khurpia in Uttarakhand

- Rajpura-Patiala in Punjab

- Dighi in Maharashtra

- Palakkad in Kerala

- Agra and Prayagraj in Uttar Pradesh

- Gaya in Bihar

- Zaheerabad in Telangana

- Orvakal and Kopparthy in Andhra Pradesh

- Jodhpur-Pali in Rajasthan

- and one additional integrated industrial node aligned with corridor expansion frameworks

These projects are connected to six major industrial corridors, including:

- Delhi-Mumbai Industrial Corridor (DMIC)

- Chennai-Bengaluru Industrial Corridor (CBIC)

- East Coast Economic Corridor (ECEC)

- Amritsar-Kolkata Industrial Corridor (AKIC)

- Bengaluru-Mumbai Economic Corridor (BMEC)

- Hyderabad-Nagpur Industrial Corridor (HNIC)

This is not random geographic distribution.

It is a deliberate economic rewiring of India’s manufacturing map.

The Strategic Context: Why NICDP Matters Now

Global manufacturing is entering its largest structural redistribution in decades.

Three powerful forces are accelerating this shift:

- China+1 diversification strategies

- Geopolitical supply-chain fragmentation

- The race for resilient manufacturing ecosystems

Multinational corporations are increasingly looking for alternative production bases capable of combining:

- scale,

- labor availability,

- logistics efficiency,

- policy stability,

- export connectivity,

- and industrial infrastructure readiness.

India has historically possessed scale and labor advantages.

What it lacked was integrated industrial execution.

NICDP is designed to close that gap.

The objective is not merely to attract factories.

The objective is to create globally competitive industrial ecosystems capable of supporting long-term export-led economic expansion.

The Indian government’s broader target of facilitating approximately $2 trillion in exports by 2030 increasingly depends on whether such industrial corridors can scale effectively.

The Core Thesis Behind the 12 Industrial Smart Cities

The NICDP model is fundamentally different from traditional industrial parks.

These projects are being developed as integrated economic ecosystems — combining:

- manufacturing zones,

- logistics hubs,

- residential infrastructure,

- commercial districts,

- warehousing clusters,

- multimodal transportation systems,

- and digital governance infrastructure.

The central strategic principle is simple:

Reduce industrial friction at every level.

That means:

- faster approvals,

- lower logistics costs,

- stable utilities,

- ready-to-operate land,

- worker accessibility,

- export connectivity,

- and urban livability.

This is why the “walk-to-work” concept is strategically important.

Industrial competitiveness is no longer only about labor cost.

It is increasingly about productivity ecosystems.

India’s New Industrial Geography

The 12 industrial smart cities are strategically distributed across key freight and manufacturing corridors to maximize logistics efficiency and regional economic integration.

Strategic Objectives of NICDP

| Strategic Lever | Expected Outcome |

|---|---|

| Plug-and-play industrial zones | Faster investment deployment |

| PM GatiShakti integration | Reduced logistics friction |

| Greenfield infrastructure | Lower retrofitting inefficiencies |

| Smart utility systems | Stable operational environment |

| Export-oriented positioning | Global manufacturing competitiveness |

| Industrial clustering | Supply-chain ecosystem formation |

| Walk-to-work urbanization | Higher workforce productivity |

| SPV-based governance | Faster execution and accountability |

The Scale of the Economic Ambition

The projected numbers surrounding NICDP are economically significant:

- Estimated investment potential: approximately ₹1.52 lakh crore

- Direct employment potential: nearly 10 lakh jobs

- Indirect employment potential: up to 30 lakh jobs

- Strategic objective: support India’s long-term export expansion ambitions

However, the real multiplier effect may emerge from secondary economic acceleration:

- logistics growth,

- housing demand,

- warehousing expansion,

- urban consumption,

- industrial financing,

- and SME ecosystem development.

Industrial corridors rarely operate as isolated economic assets.

They become regional growth multipliers.

Why “Plug-and-Play” Infrastructure Changes the Investment Equation

Historically, one of India’s largest industrial bottlenecks has been project commissioning delays.

Land acquisition uncertainty, utility approvals, connectivity gaps, environmental clearances, and infrastructure retrofitting often extended project timelines significantly.

The plug-and-play model directly targets this problem.

Under NICDP:

- trunk infrastructure is pre-developed,

- utility connectivity is pre-planned,

- transport integration is embedded,

- and operational readiness is accelerated.

For investors, this changes capital deployment dynamics.

Reduced time-to-production improves:

- project IRR,

- capital efficiency,

- manufacturing scalability,

- and operational predictability.

This is particularly critical for:

- electronics,

- semiconductors,

- EV ecosystems,

- precision manufacturing,

- logistics,

- renewable energy components,

- and export-driven industrial sectors.

The Logistics Revolution Behind NICDP

India’s logistics cost as a percentage of GDP has historically remained significantly higher than many advanced manufacturing economies.

This created structural disadvantages in export competitiveness.

NICDP’s integration with PM GatiShakti aims to address precisely this issue.

The strategic integration includes:

- highways,

- freight corridors,

- ports,

- airports,

- rail connectivity,

- and multimodal logistics systems.

The result could be a substantial reduction in:

- freight delays,

- transportation inefficiencies,

- inventory carrying costs,

- and supply-chain fragmentation.

In global manufacturing economics, logistics efficiency often determines export competitiveness as much as labor cost.

Industrial Urbanization: The Rise of Economic Cities

One of the most underappreciated aspects of NICDP is its urban development model.

India’s earlier industrial expansion frequently created disconnected industrial zones lacking social infrastructure, worker housing, healthcare systems, or commercial ecosystems.

NICDP attempts to integrate:

- industrial production,

- workforce housing,

- commercial development,

- healthcare,

- education,

- and urban services.

This is strategically important because modern manufacturing increasingly competes for skilled labor.

Cities matter to industrial competitiveness.

Livability is becoming an economic variable.

The Global Benchmarking Challenge

The success of NICDP will ultimately depend on whether these industrial smart cities can compete against:

- Shenzhen-style manufacturing ecosystems,

- Vietnamese export corridors,

- Gulf industrial free zones,

- and Southeast Asian logistics clusters.

That requires excellence across:

- execution speed,

- governance,

- policy continuity,

- logistics reliability,

- utility stability,

- labor productivity,

- and institutional coordination.

India’s opportunity is massive.

But execution discipline will determine whether NICDP becomes:

- a transformational economic platform,

or - another infrastructure ambition constrained by fragmented implementation.

Real Estate and Capital Market Implications

Industrial smart cities historically create significant secondary capital opportunities.

Potential beneficiary sectors include:

- industrial real estate,

- logistics warehousing,

- worker housing,

- data centers,

- commercial office infrastructure,

- renewable energy ecosystems,

- and urban retail expansion.

Land valuation dynamics near strategic industrial corridors could undergo structural repricing over the next decade.

Institutional investors are increasingly tracking infrastructure-led urbanization rather than traditional metropolitan expansion models.

The Geopolitical Dimension

NICDP is not merely an infrastructure strategy.

It is a geopolitical economic strategy.

As supply chains globalize away from concentrated dependence models, countries able to offer:

- resilience,

- scalability,

- export connectivity,

- and manufacturing depth

will command disproportionate economic influence.

Industrial corridors are becoming instruments of national competitiveness.

India’s long-term ambition to emerge as a global manufacturing and export powerhouse depends heavily on the success of initiatives like NICDP.

iBCV Perspective: Infrastructure Is Becoming India’s Primary Economic Multiplier

According to iBCV (iBluu Consulting Venture Private Limited), a venture of iBluu Corporations, the next phase of India’s economic transformation will likely be driven less by isolated urban growth and more by integrated industrial corridor ecosystems.

The convergence of:

- logistics infrastructure,

- industrial production,

- urban expansion,

- strategic manufacturing,

- and export-oriented planning

is creating a new framework for capital allocation in India.

The analytical depth of this perspective is aligned with the strategic lens of J Parasher, Founder and Managing Director of iBluu Corporations, whose work consistently emphasizes long-horizon industrial transformation, infrastructure competitiveness, and national capability expansion.

His perspective increasingly frames infrastructure not as a standalone construction activity, but as a strategic operating architecture capable of influencing economic resilience, export power, geopolitical leverage, and long-term capital formation.

Conclusion: India Is Entering the Era of Infrastructure-Led Industrial Strategy

The 12 industrial smart cities under NICDP may ultimately represent one of the most consequential economic infrastructure programs in India’s modern development cycle.

If executed effectively, these corridors could:

- reshape manufacturing geography,

- compress logistics costs,

- accelerate exports,

- expand industrial employment,

- and reposition India within the global supply-chain hierarchy.

The significance of NICDP is not simply that India is building industrial cities.

It is that India is attempting to build industrial systems at national scale.

And in the emerging global economic order, systems — not isolated projects — will determine long-term competitive power.

Disclaimer: This article is intended solely for informational, strategic, and analytical purposes and should not be construed as financial, investment, legal, policy, or real estate advice. The insights, projections, and viewpoints expressed are based on publicly available information, industry trends, infrastructure assessments, and independent strategic interpretation at the time of writing. Market conditions, government policies, project timelines, regulatory frameworks, and investment outcomes may change materially over time. Readers, investors, institutions, and stakeholders are advised to conduct independent due diligence and seek professional advisory before making investment, business, infrastructure, or policy-related decisions. The views expressed in this article reflect broader strategic perspectives and do not constitute guaranteed forecasts or official representations.