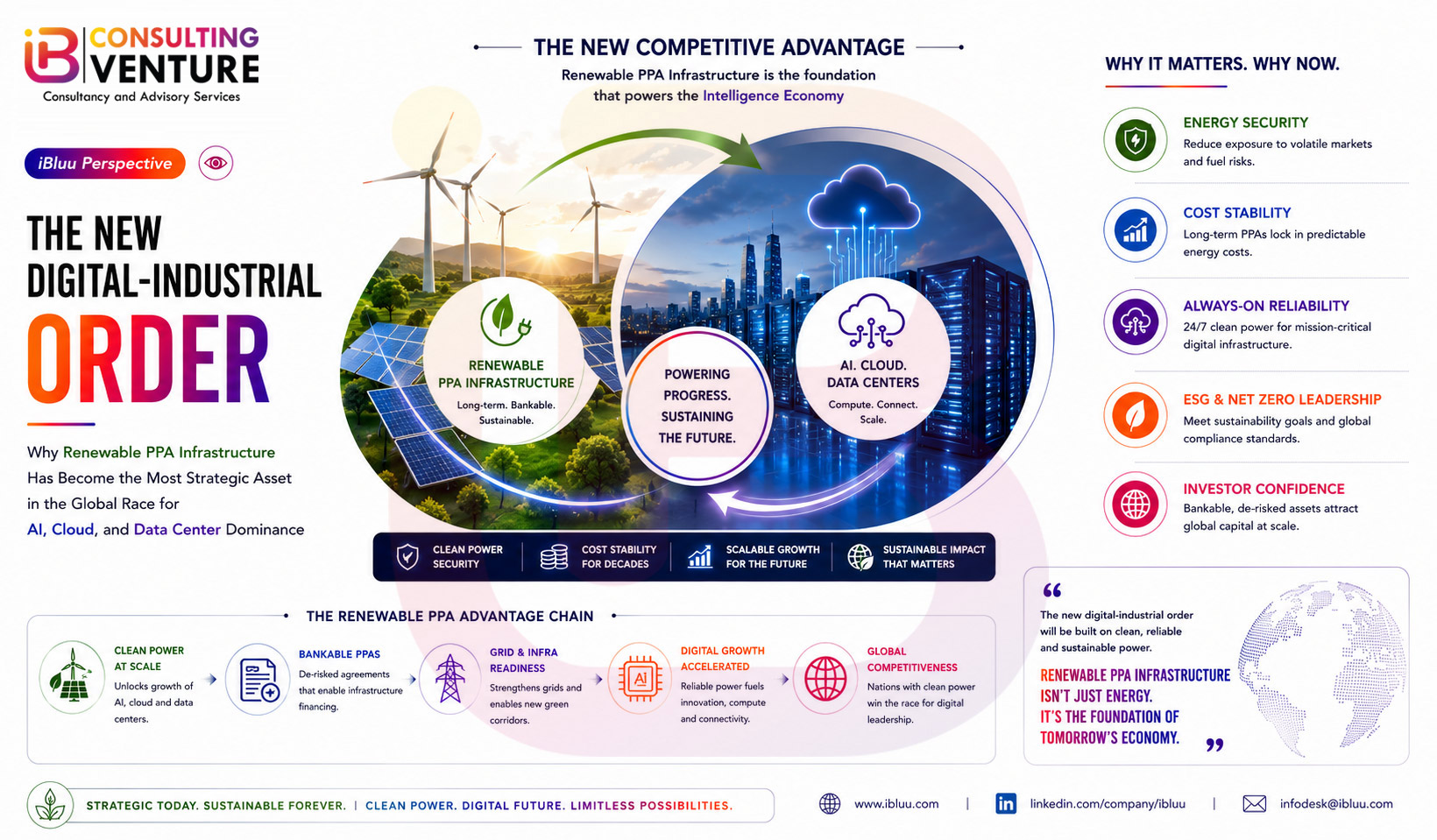

Renewable PPA Infrastructure Has Emerged as the Most Strategic Asset Powering Global Data Center Expansion, Cloud Infrastructure, and the Digital Economy

The global energy market is entering a structural transformation that extends far beyond solar parks, wind farms, or renewable capacity additions.

A new infrastructure convergence is now emerging between two of the world’s fastest-growing strategic sectors:

- Renewable Energy under long-term Power Purchase Agreements (PPAs)

- Data Center infrastructure

This convergence is rapidly reshaping how institutional capital, infrastructure investors, sovereign wealth funds, hyperscale technology companies, and renewable developers allocate billions of dollars globally.

Because the future digital economy will not be constrained by data alone.

It will be constrained by power.

And increasingly, by access to long-duration, low-cost, renewable electricity secured through strategic PPAs.

Across India, the Gulf, Southeast Asia, Europe, and North America, renewable developers are no longer looking at data centers merely as electricity consumers.

They are viewing them as:

- anchor infrastructure clients,

- long-duration contracted demand ecosystems,

- high-creditworthy counterparties,

- and strategic gateways into the next generation of digital industrial infrastructure.

The deeper reality is becoming impossible to ignore:

The next renewable energy supercycle may ultimately be driven as much by artificial intelligence and cloud computing as by climate transition policies.

The Data Center Explosion Is Creating an Unprecedented Power Demand Shock

The rise of:

- Artificial Intelligence (AI)

- Hyperscale cloud infrastructure

- Large language models

- Digital payments

- 5G ecosystems

- Edge computing

- Semiconductor manufacturing

- Industrial IoT

- Quantum computing ecosystems

has triggered one of the fastest increases in electricity demand seen in modern infrastructure history.

Globally, data centers already account for roughly 2–3% of total electricity consumption, according to estimates from the International Energy Agency (IEA). However, the next decade may fundamentally alter that equation.

By 2030:

- AI-driven data-center electricity demand could more than double globally.

- Hyperscale facilities may individually consume power equivalent to medium-sized industrial clusters.

- Data-center-linked electricity demand in major digital economies could become one of the largest incremental power-demand drivers.

The implications are enormous.

Digital infrastructure is no longer only a technology story.

It is becoming an energy-security story.

Why Renewable Energy Developers Prefer Data Centers Under PPA Structures

For renewable developers, data centers represent one of the most attractive long-term PPA counterparties in the market.

The reason is strategic, not temporary.

Data centers require:

- uninterrupted power,

- predictable energy pricing,

- ESG compliance,

- low-carbon operations,

- scalable capacity expansion,

- and long-term energy certainty.

Renewable PPAs solve all of these simultaneously.

This has created a powerful alignment between:

- renewable infrastructure developers,

- hyperscale cloud operators,

- AI infrastructure firms,

- colocation providers,

- and global infrastructure investors.

Unlike traditional industrial customers whose power demand fluctuates cyclically, data centers typically operate 24/7 with highly stable demand profiles.

That makes them exceptionally valuable from an infrastructure-financing perspective.

A long-term PPA signed with a hyperscale technology or data-center operator can transform a renewable project into:

- a bankable infrastructure asset,

- a predictable annuity-style revenue system,

- and a globally financeable platform for institutional capital.

The Global Race: Renewable Power Is Becoming a Strategic Requirement for AI Infrastructure

The world’s largest technology companies are now among the largest renewable energy buyers globally.

Major hyperscalers including:

- Amazon

- Microsoft

- Meta

have collectively signed tens of gigawatts of renewable PPAs worldwide.

Their objective is no longer limited to sustainability branding.

The strategy is operational.

AI infrastructure consumes enormous power.

And future AI competitiveness may increasingly depend on:

- access to scalable energy,

- renewable sourcing capability,

- storage integration,

- and long-term electricity cost stability.

In effect:

renewable power procurement is becoming part of technology strategy itself.

Why India Is Emerging as a Strategic Renewable + Data Center Infrastructure Hub

India is entering a unique strategic position globally because it combines:

- one of the world’s fastest-growing renewable markets,

- one of the fastest-growing digital economies,

- expanding hyperscale data-center demand,

- massive fiber and telecom growth,

- rising AI infrastructure ambitions,

- and globally competitive renewable tariffs.

India’s installed renewable energy capacity has already crossed approximately 230 GW (including large hydro) by 2026, while the country’s data-center market is projected to witness exponential growth through the next decade.

India’s total data-center capacity is expected to cross:

- 4 GW+ IT load over the medium term,

with major growth clusters emerging across: - Mumbai

- Chennai

- Hyderabad

- Noida

- Bengaluru

- Pune

- Ahmedabad

Simultaneously, renewable developers are aggressively expanding:

- solar parks,

- hybrid renewable systems,

- storage-linked projects,

- RTC renewable models,

- and open-access PPA frameworks.

The convergence between both sectors is becoming inevitable.

The Real Infrastructure Shift: From Grid Consumption to Dedicated Energy Ecosystems

The traditional power model was simple:

generate electricity → inject into the grid → consumers purchase power.

That model is rapidly evolving.

The new infrastructure architecture increasingly revolves around:

- dedicated renewable PPAs,

- captive renewable systems,

- open-access energy procurement,

- hybrid renewable + storage integration,

- and private energy ecosystems designed specifically for digital infrastructure.

Data centers increasingly prefer:

- renewable-linked PPAs,

- round-the-clock renewable supply,

- and storage-backed energy systems

to reduce exposure to volatile grid pricing and carbon-intensive electricity sources.

This is creating a completely new asset class:

Digital-energy infrastructure ecosystems.

Why Storage Is Becoming the Most Critical Layer

Solar generation alone cannot support 24/7 hyperscale infrastructure requirements.

This is why energy storage has become strategically critical.

Renewable developers heavily investing in:

- pumped hydro storage,

- battery energy storage systems (BESS),

- hybrid wind-solar systems,

- and FDRE (Firm & Dispatchable Renewable Energy)

are positioning themselves for the future data-center economy.

The next winners in renewable infrastructure may not necessarily be companies generating the cheapest electricity.

The winners may be those capable of delivering:

- uninterrupted renewable power,

- storage-backed dispatchability,

- and digitally integrated energy ecosystems.

Capital Is Following the Convergence

One of the strongest signals comes from institutional capital flows.

Global investors including:

- BlackRock

- KKR

- Brookfield

- GIC

- ADIA

- Temasek

- DigitalBridge

- EQT Infrastructure

are increasingly investing across both:

- renewable infrastructure,

- and data-center ecosystems simultaneously.

The logic is straightforward:

future digital growth requires future energy dominance.

This convergence is creating one of the most powerful infrastructure-investment themes globally.

India’s Renewable PPA Economy Could Become the Foundation of Its Digital Infrastructure Rise

India’s renewable transition is no longer only an energy-sector story.

It is becoming directly linked to:

- AI infrastructure,

- semiconductor ecosystems,

- industrial corridors,

- cloud infrastructure,

- export competitiveness,

- and long-term digital sovereignty.

As hyperscale infrastructure expands, long-term renewable PPAs may increasingly become foundational to:

- India’s digital-economy economics,

- infrastructure competitiveness,

- and technology-sector scalability.

This could fundamentally reshape:

- energy financing,

- infrastructure investment,

- industrial policy,

- and capital allocation models over the next decade.

iBCV Perspective

From the perspective of iBCV (iBluu Consulting Venture Private Limited), the convergence between renewable PPA infrastructure and data-center expansion represents one of the most strategically important infrastructure shifts of the coming decade.

The future battle is no longer only about producing electricity.

It is about controlling:

- scalable clean-energy ecosystems,

- digital infrastructure power supply,

- storage-linked dispatchability,

- and long-duration infrastructure cash flows.

As India accelerates simultaneously across:

- AI,

- semiconductors,

- manufacturing,

- renewable infrastructure,

- logistics,

- and digital infrastructure,

the integration between energy systems and digital systems will likely become structurally irreversible.

The broader analytical framework behind this perspective aligns closely with the long-horizon strategic lens often emphasized by J Parasher, Founder and Managing Director of iBluu Corporations, whose work consistently focuses on national capability creation, industrial competitiveness, infrastructure economics, and strategic transformation at scale.

Disclaimer: This article is intended solely for informational, strategic, and industry-analysis purposes. Certain projections, forecasts, capacity estimates, investment trends, and market observations are based on publicly available reports, sector analyses, industry disclosures, and forward-looking assessments available as of 2026. Actual market developments, regulatory policies, investment outcomes, and infrastructure growth trajectories may differ materially depending on economic, geopolitical, technological, and policy developments. This article should not be interpreted as financial, investment, legal, or policy advice.