Limited Partners Recalibrate Asia-Pacific: India Emerges as the New Axis of Global Private Capital

Global limited partners (LPs) have delivered a decisive signal: India is now the anchor allocation within Asia-Pacific private markets. A growing majority of institutional investors are not merely increasing exposure—they are restructuring regional strategies around India’s structural resilience, scalable growth, and improving exit ecosystem.

This is not a cyclical shift.

It is a strategic reallocation of global capital.

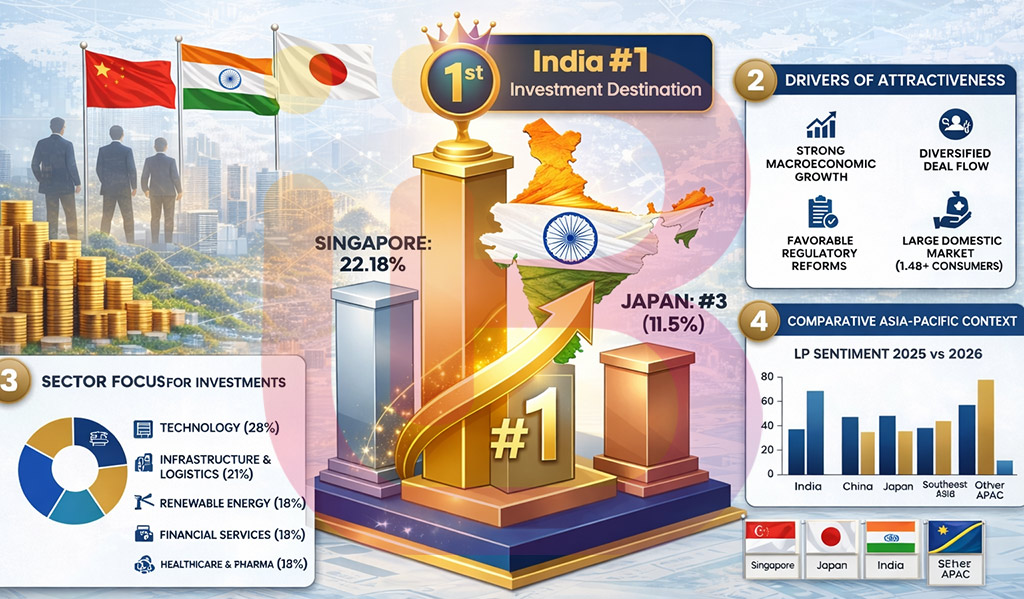

- 31% of LPs rank India as their #1 Asia-Pacific destination

- 76% place India within their top three allocations

- India commands over one-third of LP capital in the region, with European LPs allocating up to ~60% of their Asia-Pacific exposure

The implication is clear:

India has transitioned from an “emerging opportunity” to a “core portfolio market.”

The Structural Reordering of Asia-Pacific Capital Flows

For over a decade, Asia-Pacific private markets were defined by China-centric capital deployment. That paradigm is now structurally shifting.

India’s share of regional private capital has nearly doubled from ~12% (2015–2019) to ~21% (2020–2024)—even as overall regional activity moderated post-2021.

This reallocation is being driven by three decisive forces:

- Geopolitical diversification: Global LPs are actively de-risking China exposure under “China+1” strategies

- Policy predictability: India offers comparatively stable regulatory continuity and reform momentum

- Economic durability: A sustained ~7% GDP growth trajectory with domestic consumption strength

India is no longer competing within Asia-Pacific.

It is redefining the region’s capital allocation thesis.

Market Maturity: From Growth Story to Capital Efficiency Engine

India’s private markets have entered a new phase—scale with discipline.

| Metric | 2016–2020 | 2021–2025 | Shift |

|---|---|---|---|

| PE/VC Investments | ~$140B | $207B | 1.5× growth |

| Exit Value | ~$50–60B | ~$120B | >2× increase |

| Capital Intensity (% of GDP) | ~0.7% | ~1.42% | Structural deepening |

This transition signals a maturing ecosystem where:

- Exit pathways are strengthening (IPOs, secondaries, strategic sales)

- Domestic capital pools are scaling (large India-focused funds closing at $1.7–2.1B)

- Operational value creation is becoming central to returns

The market is no longer defined by entry multiples alone.

Execution quality now determines alpha.

Where LP Conviction Is Concentrated

LPs are not allocating broadly—they are concentrating capital into high-conviction sectors and strategies.

Preferred Strategies

- Buyouts (control-oriented, operational transformation)

- Growth equity (scalable mid-market champions)

High-Conviction Sectors

- Technology-enabled services

- Advanced manufacturing (PLI-led)

- Infrastructure & renewables

- Financial services

- Consumer and digital commerce ecosystems

This concentration reflects a deeper shift:

From passive capital deployment to active value creation models.

The India Advantage: Structural, Not Tactical

India’s investment appeal is anchored in multi-decade structural drivers:

- Demographic leverage: Young workforce, expanding middle class

- Digital public infrastructure: UPI, Aadhaar, ONDC enabling scalable business models

- Manufacturing resurgence: PLI schemes accelerating domestic production

- Consumption expansion: Rising income elasticity across sectors

Unlike many emerging markets, India offers simultaneous growth across consumption, infrastructure, and industrial transformation.

This creates portfolio diversification within a single geography—a rare advantage at scale.

Scenario Modeling: Capital Deployment Through 2030

| Scenario | Deployment Growth (CAGR) | Key Drivers | Probability |

|---|---|---|---|

| Base Case | 15–20% | Sustained growth, stable policy, strong exits | Highest |

| Upside Case | 25%+ | Accelerated reforms, capital shift from China | 35–45% |

| Downside Case | 5–10% | Global shocks, valuation compression | 20–30% |

Key Insight:

Even in downside scenarios, India maintains positive capital deployment growth, underscoring structural resilience.

Risk Landscape: Conviction with Discipline

LP optimism is tempered by rigorous risk assessment:

- Valuation risk: Potential 15–25% compression in downside scenarios

- Execution risk: Gaps in operational transformation capabilities

- Regulatory evolution: FDI norms, taxation clarity, data localization

- Liquidity cycles: Exit timing and market depth variability

However, these risks are not deterrents—they are pricing variables.

The most sophisticated LPs are not reducing exposure.

They are demanding higher execution quality.

The Winning Playbook: What Differentiates Top-Performing GPs

The next phase of India’s private markets will reward operational excellence over financial engineering.

Five defining capabilities:

- Sectoral depth with execution edge

- Institutional-grade governance and ESG integration

- Multi-path exit design from entry stage

- Local execution with global best practices

- Dynamic portfolio construction across cycles

LP capital is increasingly flowing toward GPs that can institutionalize these capabilities.

Actionable Recommendations

For Limited Partners

- Increase India allocation to 25–40% of Asia-Pacific exposure

- Prioritize buyout and growth strategies with operational control

- Stress-test portfolios for 15–25% downside scenarios

- Mandate ESG and governance transparency at fund level

For General Partners

- Build clear India-differentiated investment theses

- Invest heavily in post-acquisition value creation capabilities

- Expand pipelines in manufacturing, tech services, and green infrastructure

- Enhance LP reporting transparency and co-investment structures

Bold Moves for 2026–2030

- Launch dedicated India buyout platforms targeting mid-market control deals

- Integrate AI-driven due diligence and portfolio analytics

- Deepen partnerships with domestic institutions and family offices

- Build sector-focused platforms aligned with national priorities

Conclusion: From Allocation Choice to Strategic Imperative

India’s rise in LP portfolios is not a momentum trade.

It is a strategic redefinition of Asia-Pacific capital allocation.

The convergence of growth durability, policy continuity, and improving capital market depth positions India as a long-term compounding engine for global investors.

However, the next phase will not be won by capital alone.

It will be won by discipline, execution, and strategic clarity.

Final Word

India is no longer an emerging market bet.

It is a core allocation market with asymmetric upside potential.

Those who approach it with rigor, patience, and operational precision will not just participate in growth—

They will define the next decade of private capital leadership in Asia-Pacific.

Disclaimer: This analysis is based on publicly available data and industry benchmarks as of 2026. It is intended for informational purposes only and does not constitute investment advice. Actual outcomes may vary based on market conditions, regulatory developments, and execution factors.