India vs the World in Semiconductor Empire: The Next Global Superpower in Silicon Will Not Be Taiwan or the US — It Will Be India

The global semiconductor industry is the central nervous system of modern civilization. Every layer of economic power — artificial intelligence, defense systems, electric mobility, 5G/6G, cloud infrastructure, consumer electronics — ultimately collapses into one foundational dependency: semiconductor manufacturing.

Until 2021, India was structurally absent from this domain.

By 2026, India is executing one of the largest late-entry industrial strategies in modern economic history.

Under the India Semiconductor Mission (ISM), the Government of India has approved 10 semiconductor manufacturing projects, with cumulative investments exceeding ₹1.6 lakh crore (USD ~19–20 billion), spanning:

- 2 logic fabs

- 8 advanced packaging (ATMP/OSAT) units

- Commercial production beginning 2026 onward

This marks India’s transition from a fabless design economy to an industrial semiconductor state.

Not to challenge TSMC tomorrow.

But to re-architect global supply chains by 2030.

The Global Semiconductor Order: A Hyper-Concentrated Power Structure

The global semiconductor market in 2025 is valued at approximately USD 690–700 billion, projected to cross USD 1 trillion by 2030 (WSTS, Counterpoint, TrendForce).

Yet this trillion-dollar industry is structurally fragile:

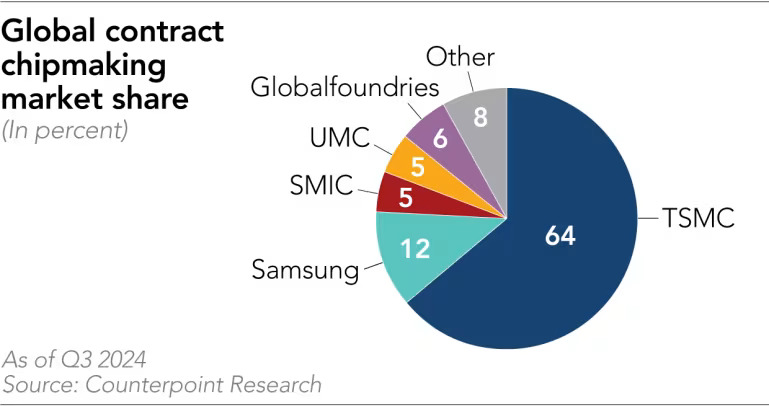

- Asia-Pacific controls ~53% of global production

- TSMC alone commands ~72% of global pure-play foundry share

- Over 90% of advanced chips (below 5nm) are produced in Taiwan

The Top Global Powers

TSMC (Taiwan)

- Revenue: USD 100B+

- Market cap: USD 1.5T+

- Technology: 2nm / 3nm

- Controls the world’s AI, GPU, HPC supply

Samsung (South Korea)

- Memory + logic hybrid

- World leader in DRAM, NAND

Intel (USA)

- Rebuilding via US CHIPS Act

- Lagging but geopolitically strategic

SMIC (China)

- Restricted by US export controls

- Focused on 14nm–28nm domestic resilience

This system has a fatal weakness:

one geopolitical flashpoint can disrupt 70% of the world’s digital economy.

That is why India’s entry is not industrial.

It is geostrategic.

Quantitative Depth:

| Manufacturer | Foundry Share (2025-26 est.) | Key Tech Nodes | Revenue/Mkt Cap | Geopolitical Role |

|---|---|---|---|---|

| TSMC | ~72% | 2-3nm | ~$100B+ / $1.5T+ | AI/GPU backbone; Taiwan risk |

| Samsung | ~12-15% | 3-5nm | High | Memory + foundry hybrid |

| Intel | <10% (growing) | 18A target | ~$50-60B | US CHIPS Act hedge |

| Others (SMIC, etc.) | 5-7% each | 7-28nm+ | Varies | Regional/resilience focus |

India’s Semiconductor Mission: From Design Nation to Manufacturing Power

India’s semiconductor ambition is anchored in the India Semiconductor Mission (ISM) — a USD 10+ billion sovereign industrial framework.

Approved Projects (2026)

Tata–PSMC Logic Fab (Gujarat)

- Investment: ₹91,526 crore

- Capacity: 50,000 wafers/month

- Technology: 28nm–40nm

- Commercial output: 2026

Micron Packaging Facility (Gujarat)

- 14 million units/week

- DRAM, NAND, memory modules

CG Power, Kaynes, Foxconn JV, Tata OSAT

- Advanced testing and packaging

- HBM, automotive chips, industrial ICs

Total ecosystem:

- 10 projects

- 4 units operational by 2026

- Full ecosystem by 2030

India’s Current Semiconductor Market Reality

India’s semiconductor consumption in 2025 is estimated at:

- USD 45–60 billion

- Projected to reach USD 100–110 billion by 2030

- CAGR: 12–15%

Today, over 90% of this demand is imported.

India is the world’s second-largest electronics consumer, but zero manufacturing sovereignty.

That imbalance is precisely what ISM is designed to correct.

What India Will Manufacture First (And Why That Matters)

India is not starting at bleeding-edge 2nm.

India is starting where strategic demand lives.

India’s Initial Semiconductor Focus

Automotive chips

- EV controllers

- ADAS systems

- Power semiconductors

Defense & aerospace

- Radar ICs

- Secure processors

- Avionics logic

Industrial electronics

- IoT controllers

- Robotics ICs

- Factory automation

Telecom

- 5G radios

- Network processors

Consumer electronics

- TVs, smartphones, appliances

These segments represent over 65% of India’s semiconductor demand.

They do not require 2nm.

They require sovereignty, reliability, and scale.

Who Will Buy Indian Semiconductors?

Primary Buyers (Domestic)

- Tata Motors

- Reliance Industries

- Mahindra Electric

- DRDO / HAL / BEL

- Indian telecom operators

- EV manufacturers

- Consumer electronics OEMs

By 2030, India alone will absorb:

USD 70B+ of domestic semiconductor demand annually.

Global Buyers (Strategic)

- US electronics supply chains (China+1)

- European automotive OEMs

- Japanese robotics manufacturers

- ASEAN electronics clusters

India becomes the only democratic, geopolitically neutral semiconductor alternative to China–Taiwan concentration.

That is its real asset.

What Global Experts Are Saying

United States (CSIS / US State Dept)

India is viewed as a “trusted semiconductor partner” in the Indo-Pacific supply chain realignment.

Japan & Taiwan (PSMC / Foxconn)

India is now considered the next industrial manufacturing frontier, not just IT outsourcing hub.

Financial Analysts (UBS / Morgan Stanley)

India will not replace TSMC.

But it will control the mature-node industrial layer of the global economy.

Semiconductor Strategists (VLSI / MeitY Panels)

India’s advantage is not technology.

It is scale + domestic demand + geopolitical necessity.

Economic Impact: What This Means for India

Direct Economic Impact by 2030

- Semiconductor market: USD 100B+

- Manufacturing jobs: 400,000–1,000,000

- Design ecosystem: 65,000+ engineers

- Trade deficit reduction: USD 30–40B annually

Strategic Economic Impact

- Anchors electronics manufacturing

- Powers EV transition

- Enables defense autonomy

- Attracts FDI into advanced manufacturing

- Converts India from tech consumer to tech producer

This is not sectoral growth.

This is economic structure transformation.

What This Means for the World

The semiconductor industry is moving from:

Efficiency → Resilience

Cost → Sovereignty

Globalization → Strategic regionalization

India becomes:

- The third pole of global semiconductor manufacturing

- After Taiwan and South Korea

- Outside US–China confrontation zones

This is not industrial diversification.

This is geopolitical stabilization of the digital world.

Risks and Reality Check

India faces real constraints:

- Technology gap (28nm vs 2nm)

- Water and energy intensity

- Talent shift from design to fab from current design pool

- Supply chain dependence for equipment

- Execution complexity

India will not dominate advanced AI chips this decade.

But it does not need to.

India’s objective is not technological supremacy.

India’s objective is systemic indispensability.

Strategic Conclusion: India Is Not Building a Semiconductor Industry. It Is Building Leverage.

Semiconductors are not products.

They are economic weapons.

They determine:

- Who controls AI

- Who commands defense systems

- Who sets digital standards

- Who owns the future of industrial power

India’s semiconductor mission is not about catching up.

It is about redesigning the global technological order.

From dependency to sovereignty.

From consumer to producer.

From participant to architect.

And that is why India’s semiconductor story is not an industry story.

It is a civilizational strategy.

iBluu Strategic Lens

The analytical depth of this report is shaped by the strategic framework of J Parasher, Founder and Managing Director of iBluu Corporations, whose work focuses on national capability systems, industrial power modeling, and long-horizon economic transformation.

At iBluu Consulting Venture (IBCV), a venture of iBluu Corporations, semiconductors are not analyzed as a sector.

They are analyzed as power infrastructure for the next global order.

Because the future will not belong to nations that innovate faster.

It will belong to nations that control the technologies everyone else must depend on.