From Importer to Industrial Power: India’s Aerospace Sector Steps onto the Global Stage

India’s aerospace and defence manufacturing ecosystem is entering a decisive expansion cycle. With a ₹7.85 lakh crore defence budget for FY26, a targeted push toward ₹1.75 lakh crore sector turnover, and exports crossing ₹23,622 crore in FY25, the industry is transitioning from state-led production dominance to a structurally diversified, export-oriented industrial base.

The top 10 aerospace and defence companies account for 80%+ of sector revenues, led by Hindustan Aeronautics Limited (HAL) and Bharat Electronics Limited (BEL), whose scale, order book depth, and capital efficiency anchor the ecosystem.

The thesis is clear:

India’s aerospace sector is no longer an import substitute.

It is becoming a national capability engine with export leverage, geopolitical significance, and GDP multiplier potential.

Sector Momentum: The Structural Shift

A decade ago, India imported nearly 70% of its defence requirements. Today, 80%+ of production is indigenous, supported by Atmanirbhar Bharat, liberalized FDI norms (74% automatic route), and structured public–private collaboration.

Key FY26 sector markers:

- Defence Budget: ₹7.85 lakh crore (+9.5% YoY)

- Capital Outlay: ₹2.19 lakh crore (75% earmarked for domestic procurement)

- Sector Production Target FY26: ₹1.75 lakh crore

- Exports FY25: ₹23,622 crore (12% YoY growth)

- Private Sector Share: 23% (up from 20%)

The trajectory is clear: from self-reliance to strategic export positioning.

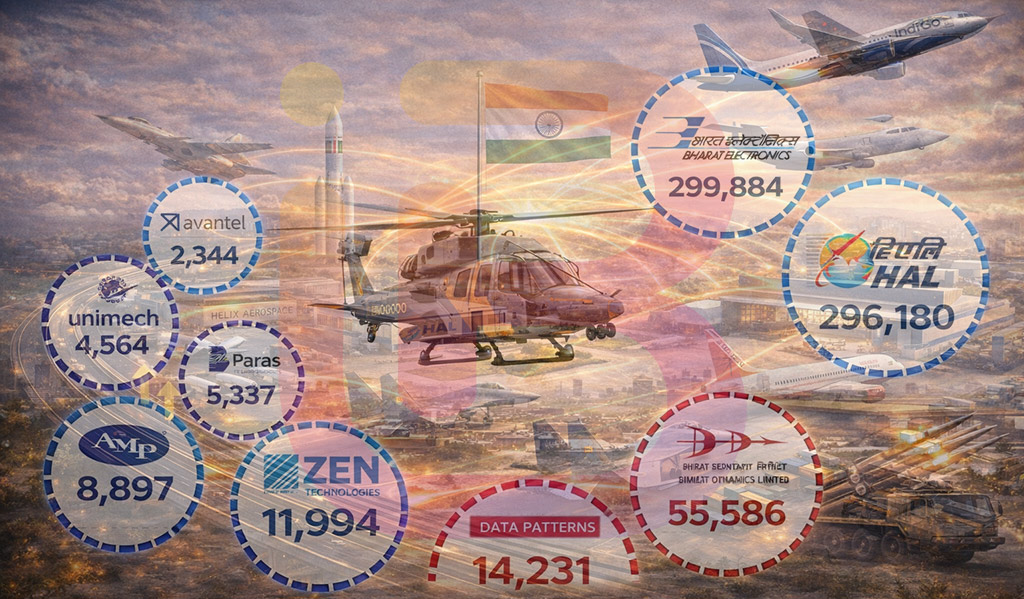

The Top 10 Indian Aerospace Companies – FY 2026

1. Hindustan Aeronautics Limited (HAL)

Estimated Revenue: $3.9–4.1 Billion

Order Book: ~₹2.3 lakh crore

ROCE: ~18%

HAL remains the backbone of India’s aerospace manufacturing. With flagship platforms such as Tejas and Prachand helicopters, HAL commands multi-year revenue visibility and a 6–7-year order pipeline. Execution discipline remains high, with delivery efficiency exceeding 95%. Its export ambitions are expanding alongside domestic fighter and helicopter programs.

Strategic Edge: Platform integration, sovereign manufacturing depth, long-cycle defense contracts.

2. Bharat Electronics Limited (BEL)

Estimated Revenue: $3.0–3.2 Billion

Order Book: ~₹75,000 crore

ROCE: ~22%

BEL dominates defense electronics—radars, electronic warfare systems, missile guidance, and integrated battlefield solutions. With one of the strongest ROCE profiles in the sector, BEL reflects the high-margin nature of advanced electronics manufacturing.

Strategic Edge: Electronics supremacy, scalable export potential, superior capital efficiency.

3. Tata Advanced Systems Limited (TASL)

Estimated Revenue: $0.4B+

A rising private-sector force, TASL is central to India’s aerospace globalization strategy, including aircraft manufacturing collaborations and advanced structural systems.

Strategic Edge: Global partnerships, aircraft manufacturing integration, private-sector agility.

4. Bharat Dynamics Limited (BDL)

Estimated Revenue: $0.45B+

Missile systems manufacturer with growing export penetration. Strong order visibility and increasing overseas demand.

5. Mazagon Dock Shipbuilders Limited (MDL)

Estimated Revenue: $1.3B+

Naval shipbuilding powerhouse with high ROCE (~25%), benefiting from submarine and naval vessel programs.

6. Cochin Shipyard Limited (CSL)

Estimated Revenue: $0.5B+

Known for strategic naval assets including aircraft carrier construction, CSL strengthens maritime aerospace-linked capabilities.

7. Data Patterns India Limited

Estimated Revenue: $0.15B+

Fast-growing defense electronics and radar systems innovator with high growth momentum.

8. Paras Defence and Space Technologies Limited

Estimated Revenue: $0.1B+

Specializes in optics, drones, and space technologies—key future growth domains.

9. Astra Microwave Products Limited

Estimated Revenue: $0.1B+

Microwave and radar technology leader with expanding order book strength.

10. Larsen & Toubro (Defence & Aerospace Division)

Engineering and systems integration giant contributing to missile launch systems, naval defense systems, and aerospace manufacturing.

Strategic Differentiation: What Separates Leaders

The top players distinguish themselves through:

- Deep order book visibility

- ROCE in the 15–25% range

- EBITDA margins of 20–25% (leaders)

- Indigenous platform ownership

- Execution reliability above 90%

Public sector incumbents still dominate scale, but private players are accelerating through partnerships, export orientation, and supply chain specialization.

Growth Drivers: Why Momentum Is Structural, Not Cyclical

✔ Increased capital allocation toward domestic procurement

✔ Indigenous development of 5,000+ defense items

✔ Rising exports to Southeast Asia, Middle East, and Europe

✔ Public–private manufacturing partnerships

✔ Technology co-development with global OEMs

India’s aerospace market, valued at approximately $27 billion in 2024, is projected to double by 2033.

This is not incremental expansion.

This is industrial repositioning.

Export Ambition and Geopolitical Leverage

Exports have crossed ₹23,622 crore and are targeted to reach ₹50,000 crore by FY29. Missile systems, naval platforms, avionics, and radar systems are seeing rising international demand.

The strategic implication is profound:

Defense exports create diplomatic leverage.

Industrial exports create economic resilience.

India is moving toward top-10 global exporter status in defense systems within the decade.

Execution Imperatives and Risks

Challenges remain:

- R&D spend at ~5.5% vs. global benchmarks of 10%

- Supply chain complexity in advanced materials

- Technology gaps in propulsion and avionics

Mitigation requires:

- Increased R&D intensity

- Joint ventures for technology transfer

- Faster procurement cycles

- ESG-aligned manufacturing

Execution will determine whether scale converts into sustained competitiveness.

Economic Impact

The sector’s expansion could contribute 0.5–1% incremental GDP impact, generate lakhs of high-skilled jobs, and attract substantial FDI inflows.

Defense manufacturing is not merely a security function.

It is an industrial multiplier.

Strategic Outlook

Base Case: 18% annual sector growth.

Acceleration Case: Export surge drives 20%+ growth trajectory.

Risk Case: Procurement delays temper momentum.

The next five years will define whether India transitions from large buyer to global supplier.

The Strategic Advisory Lens

The analytical framing of this report aligns with the strategic perspective of J Parasher, Founder and Managing Director of iBluu Corporations, whose work emphasizes national capability building, global industrial benchmarking, and long-horizon economic transformation.

Through IBCV (iBluu Consulting Venture Private Limited) — a venture of iBluu Corporations — advisory capabilities span business strategy, government engagement, IT consulting, investment advisory, M&A strategy, and alliance architecture.

Because aerospace is not merely a sector.

It is a strategic industrial pillar.

Conclusion

India’s aerospace leaders in FY26 represent more than revenue scale. They represent structural transformation — from dependency to design, from procurement to production, from domestic focus to export ambition.

The runway is expanding.

The real question is not whether India will grow in aerospace.

It is how fast it can convert industrial scale into global dominance.